📊 Daily Market Intelligence Report

Monday, August 10, 2026

7:00 AM CST

📊 Top-Line Summary

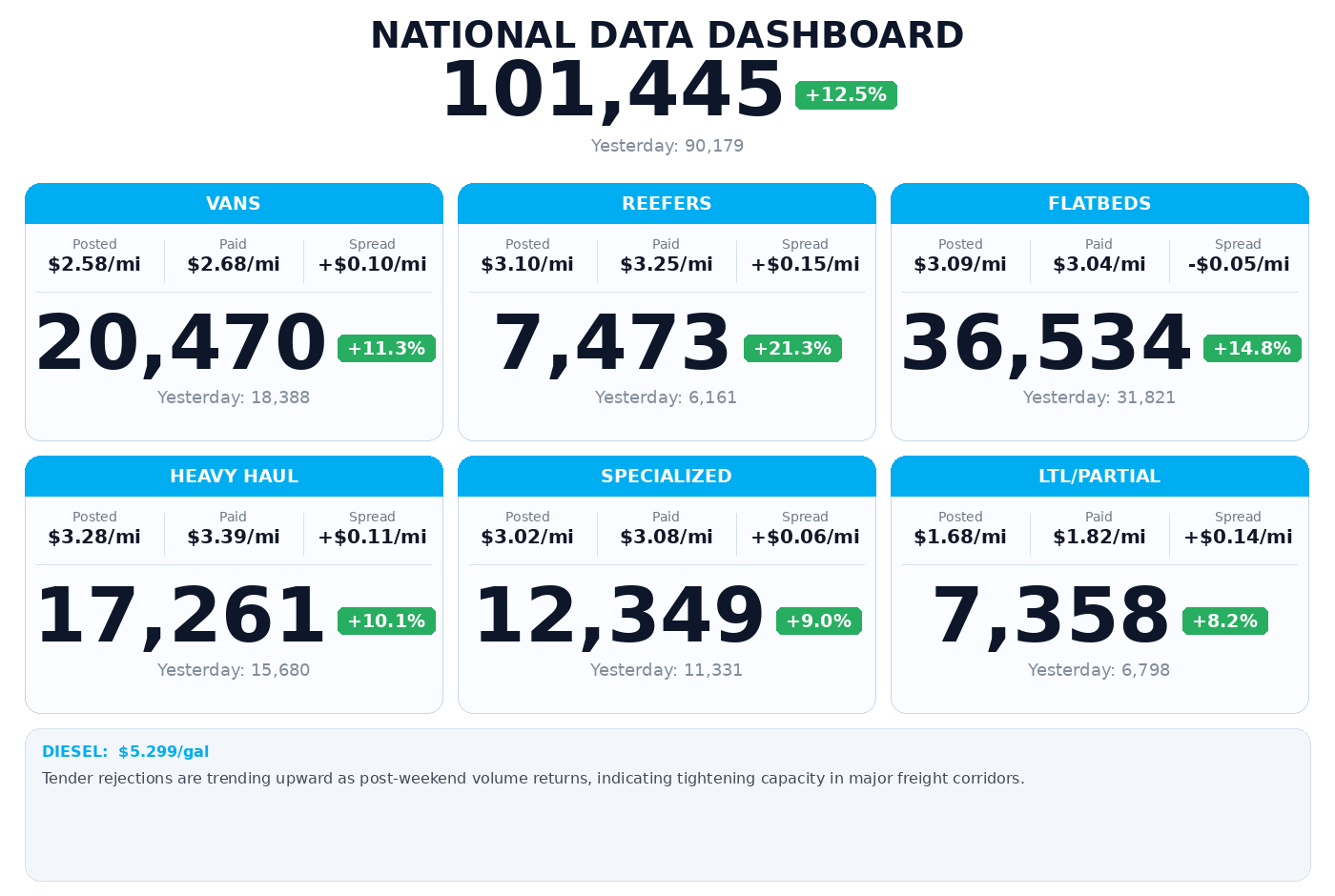

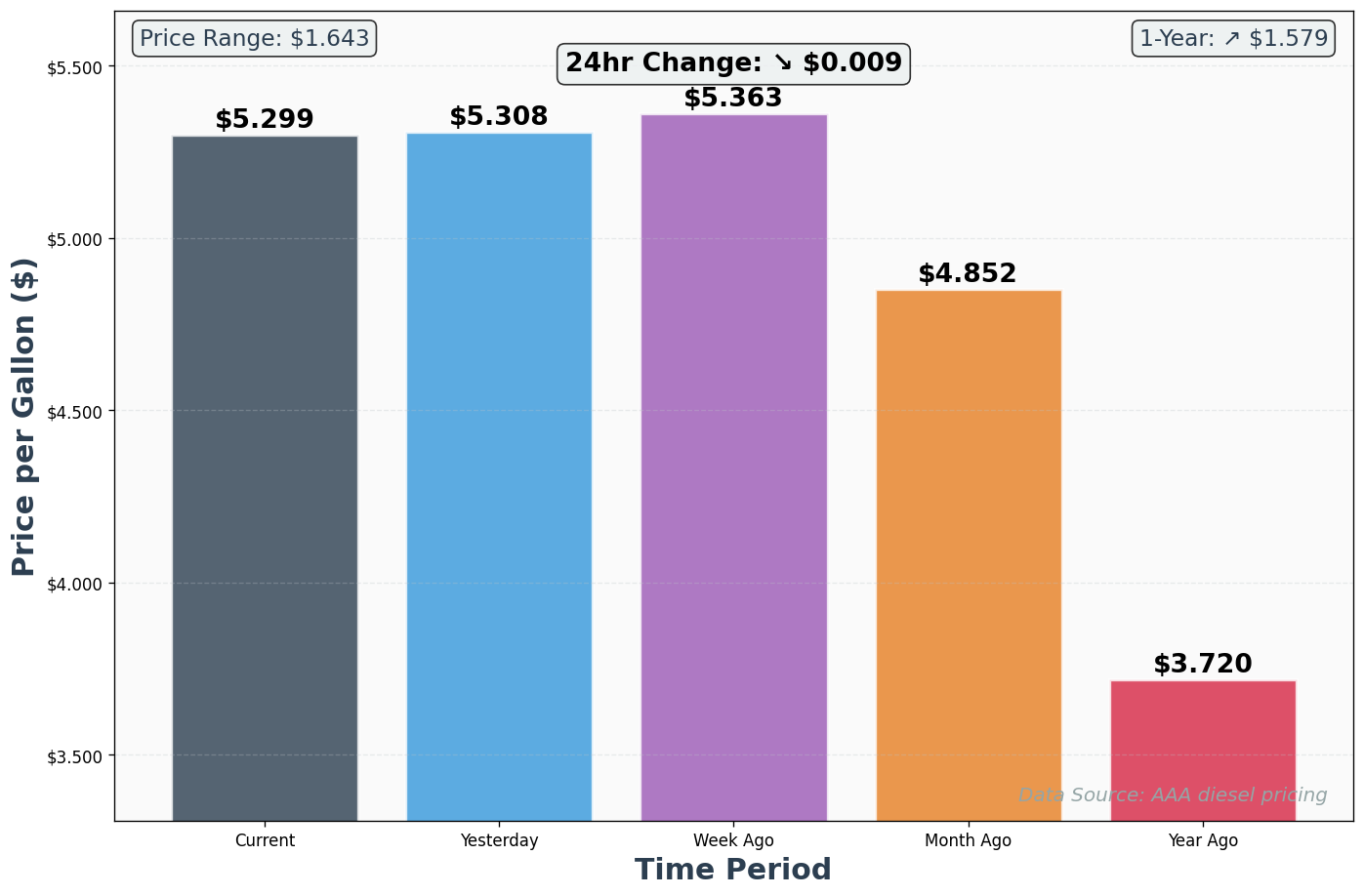

On Monday, August 10, 2026, the domestic spot market experienced a sharp post-weekend volume rebound, with total available loads surging 12.5% overnight to 101,445. The market average rate climbed to $2.83/mile, supported by AAA diesel holding at $5.299/gallon, which continues to act as a rigid floor for carrier operating costs. Extreme heat warnings across the Southwest and Midwest are straining driver hours and equipment, while peak summer produce harvests drive intense competition for temperature-controlled capacity. For brokers, the current environment offers strong margin opportunities, particularly in the Southeast and Midwest where seasonal demand and capacity imbalances allow for strategic rate negotiation.

Insight

Paid-market strength suggests intraday repricing risk

The paid-over-posted spread across van, reefer, and specialized equipment signals that load board quotes are still catching up to live carrier expectations. Same-day freight is most exposed to afternoon repricing as carriers commit early to shorter, higher-yield reloads and become less tolerant of unpaid dwell or deadhead.

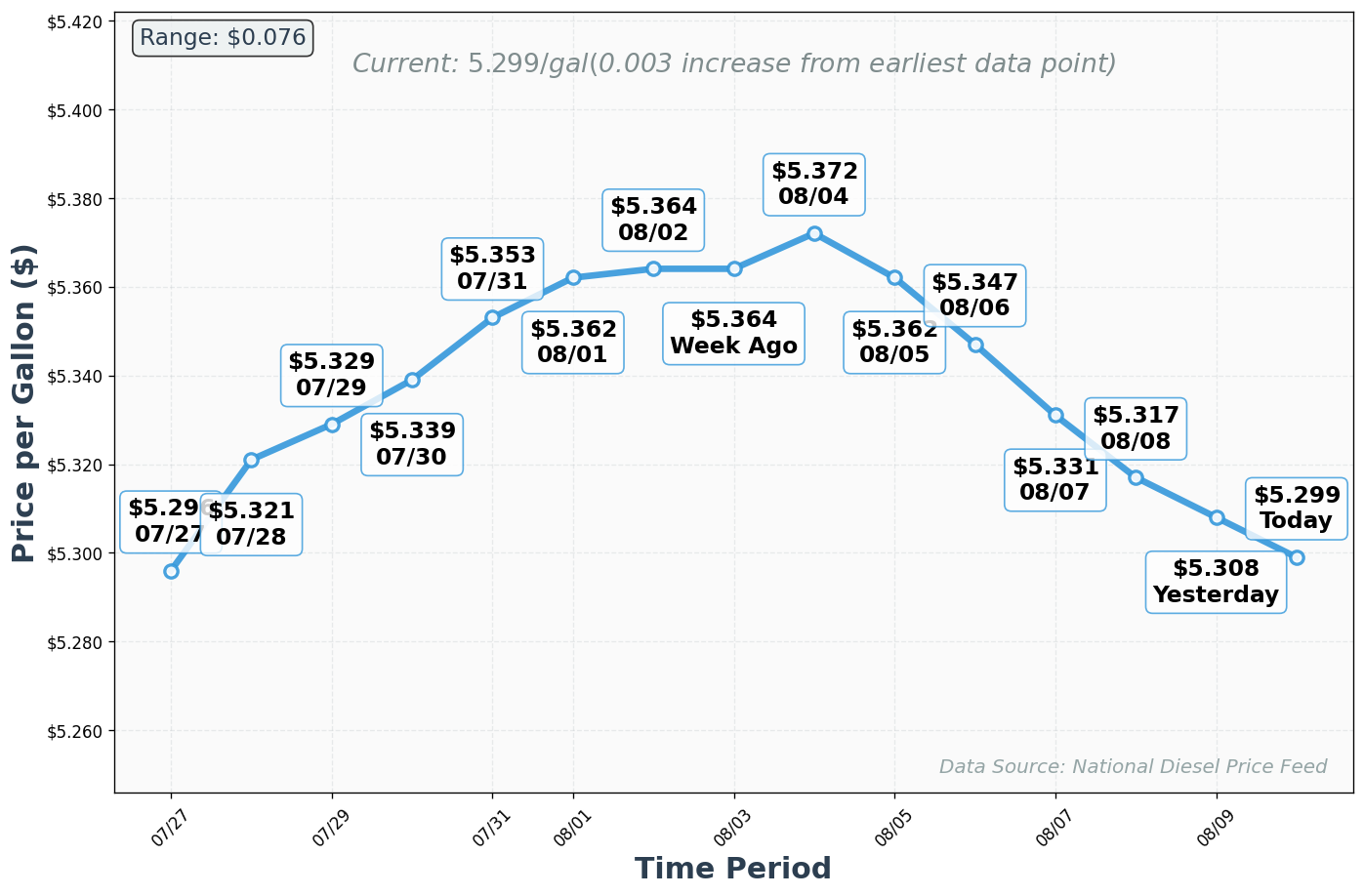

⛽ Diesel Price Analysis

Diesel Historical Price Comparison

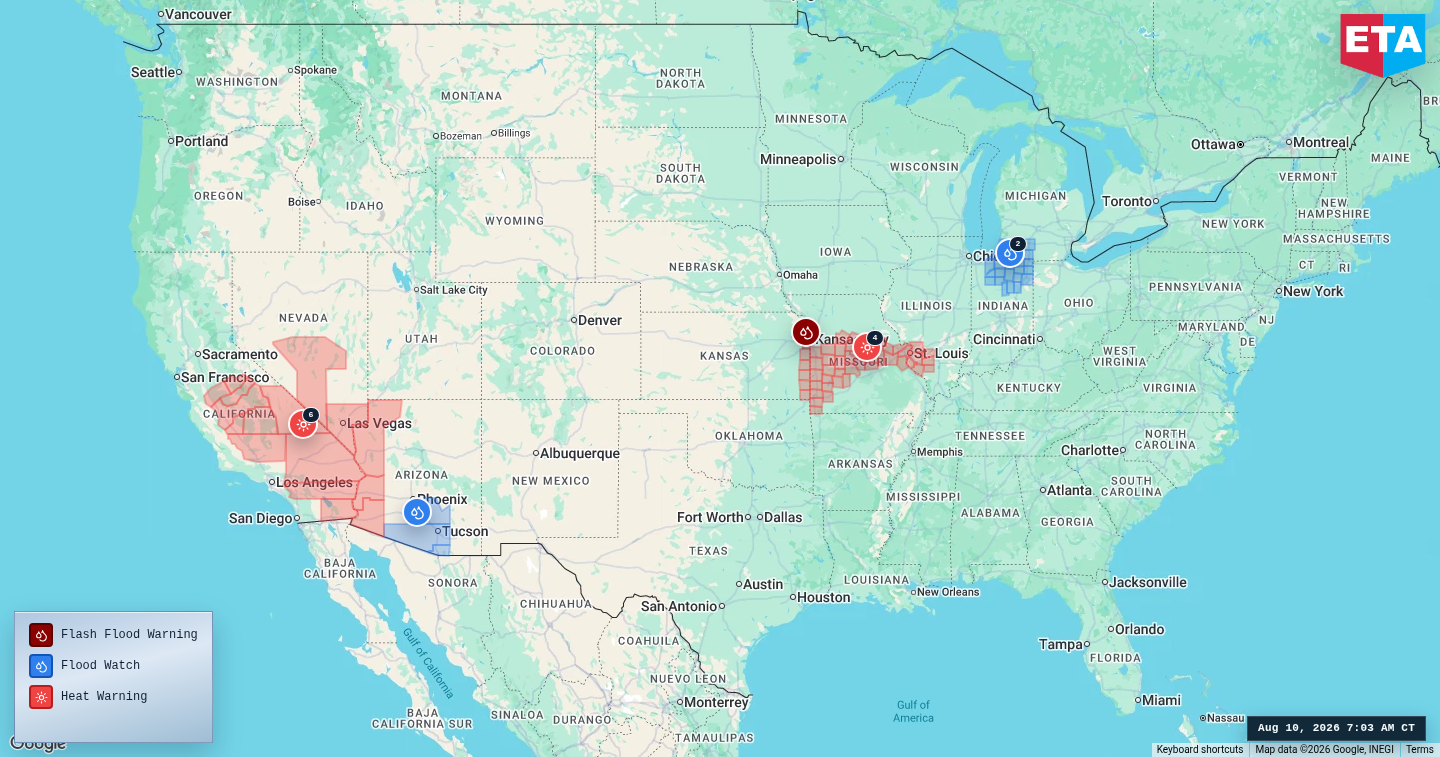

🌦️ Weather & Seasonal Intelligence

Current Major Weather Events:

- Flash Flood Warning (Midwest (KS, Johnson County)): Heavy rainfall of 2 to 3 inches has caused ongoing flash flooding of small creeks, streams, urban areas, highways, and underpasses. This may disrupt local freight operations and delay transit along the I-35 corridor near Overland Park and Olathe.

- Extreme Heat Warning (Southwest and West Coast (AZ, CA, NV)): Dangerously hot conditions with temperatures up to 115 degrees are expected. This extreme heat poses severe risks of equipment failure, particularly for reefer units, and may limit driver hours of service due to safety concerns along the I-10, I-15, and I-40 corridors.

- Extreme Heat Warning (Midwest (IL, MO)): Dangerously hot conditions with heat index values up to 111 degrees are expected through Wednesday evening. High humidity and extreme heat increase the risk of heat-related illnesses, potentially slowing down loading and unloading operations at facilities along the I-70, I-64, and I-55 corridors.

- Extreme Heat Warning (Central Plains (KS, MO)): Dangerously hot conditions with heat index values up to 108 degrees are expected through Wednesday evening. This may impact driver safety and slow down freight handling at regional distribution centers along the I-35 and I-70 corridors.

Weather Affected Corridors:

Weather Insight

Kansas City freight faces a flood-to-heat handoff

Around Johnson County, the operational risk shifts from overnight flooding into dangerous afternoon heat, creating a two-stage disruption along the I-35/Kansas City metro network. Local pickups, final-mile moves, and cross-dock handoffs near Overland Park and Olathe are the most likely pain points, with recovery slowed by 106-108 degree conditions after the morning window.

- Prioritize morning pickups and avoid tight same-day transfer commitments in the south Kansas City metro.

- Expect detention disputes to rise if drivers are held through the hottest part of the afternoon.

Weather Insight

Southwest heat remains a duration problem, not a one-day spike

California, Arizona, and Nevada stay hot through Tuesday, keeping reefer and open-deck capacity sticky on the I-10, I-15, and I-40 corridors. The biggest brokerage consequence is not road closure risk but service degradation: longer pre-cool times, more conservative dispatching, and reduced willingness to accept afternoon loading appointments at outdoor facilities.

- Morning loading windows will clear faster than late-day appointments.

- Pre-cool, idling, and heat-related equipment risk premiums are likely to hold through tomorrow.

💰 Financial Market Indicators

- Diesel Futures: Diesel futures remain elevated, reflecting ongoing global supply pressures and keeping carrier fuel surcharges high.

- Carrier Financial Health: Small carrier margins remain under pressure due to high operating costs, driving continued market consolidation and capacity exits.

- Economic Indicators: Robust consumer demand and early peak-season import volumes continue to support domestic freight demand.

📰 Impactful News Analysis

-

Matson Q2 Earnings Highlight Robust Transpacific Demand and Elevated Freight Rates 🔗:

Matson's strong Q2 results, driven by tight market conditions and robust demand in its China service, suggest that elevated ocean freight rates and volumes are likely to persist. For domestic brokers, this indicates a continued influx of import volumes at West Coast ports, which will drive strong demand for outbound drayage and truckload capacity. Brokers should prepare for sustained volume pressure and coordinate with carriers to secure capacity early.

-

New Freight Brokers Urged to Focus on Relationships and Cash Flow in First 90 Days 🔗:

Industry guidance emphasizes the critical importance of relationship building, carrier vetting, and cash flow management for new freight brokerages. In a highly competitive market, brokers who prioritize service quality and carrier compliance over low rates are better positioned to build sustainable businesses. This highlights the ongoing need for strict carrier vetting to mitigate liability risks and ensure operational reliability.

-

Boca Raton Infrastructure Construction Alters Local Traffic Patterns 🔗:

Critical water utility upgrades near Olympic Heights High School in Boca Raton, FL, will alter traffic patterns and restrict access to local roads. While localized, this construction will cause delays for regional delivery trucks and service vehicles in Palm Beach County. Brokers managing local deliveries should advise carriers to expect delays and plan alternative routes.

News Insight

Matson strength points to inland rate pressure later this week

Sustained transpacific demand is likely to show up first as tighter Southern California transload and drayage conditions, then spill inland as firmer eastbound dry van pricing several days later. That pattern usually makes outbound West Coast capacity less negotiable before it materially lifts rates in inland destination markets, giving brokers a short window to secure eastbound coverage ahead of the next import-driven push.

🗺️ Regional & Lane Analysis

📍 Primary Region Focus: Southeast US

The Southeast remains the most strategically important region today, driven by peak summer produce harvests and robust regional manufacturing activity. Reefer capacity is exceptionally tight as carriers prioritize high-paying agricultural loads, driving outbound rates up. Dry van capacity is also tightening as retail distribution centers ramp up shipping. Brokers can capitalize on these conditions by securing capacity early and leveraging inbound lanes to negotiate favorable backhaul rates.

🛣️ Key Lane Watch

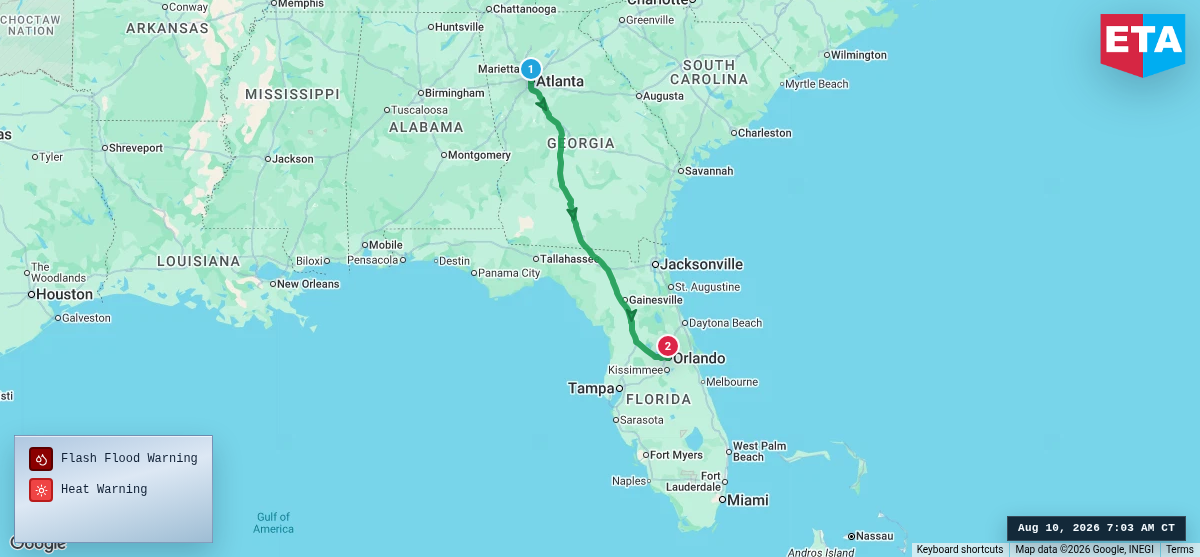

Atlanta, GA → Orlando, FL: This lane is experiencing high volume as retail and food service distribution centers in Florida pull inventory from Atlanta hubs. Reefer capacity is particularly tight due to the seasonal demand for temperature-controlled goods. Dry van demand is also strong, with rates firming as post-weekend shipping resumes.

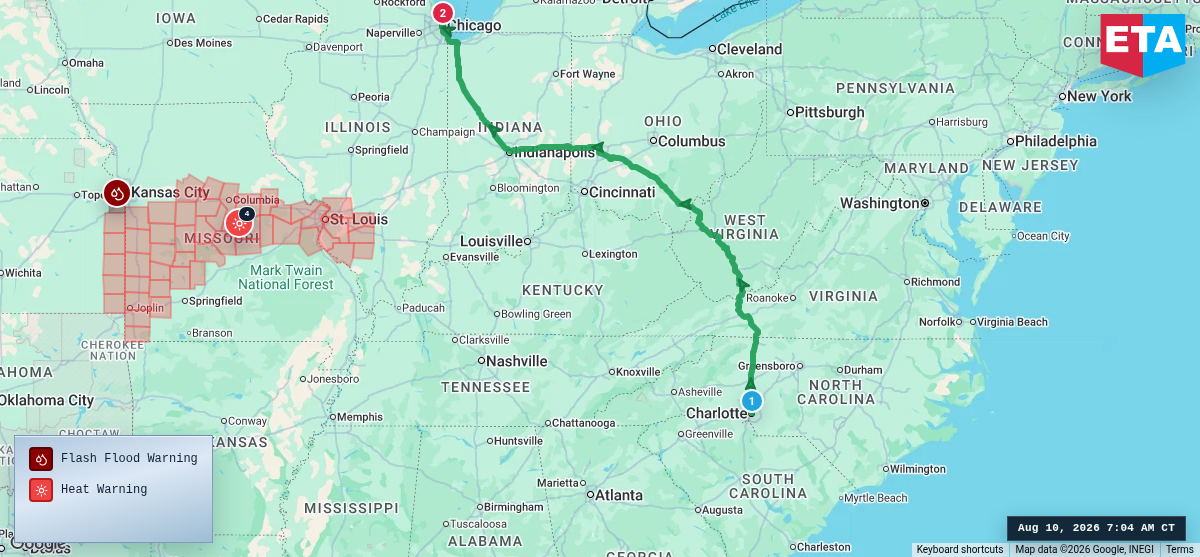

Charlotte, NC → Chicago, IL: This major manufacturing and distribution lane is seeing steady volume growth. Dry van capacity is balanced, but rates are firming as carriers seek to cover high fuel costs on longer hauls. Flatbed demand is also active, supported by regional construction projects.

Regional Insight

Atlanta-to-Florida coverage will hinge on the return leg

Atlanta-to-Orlando freight is colliding with Southeast produce repositioning, which is pulling reefers toward Georgia and South Carolina before they head into Florida. The squeeze is less about pure outbound demand than reload economics: carriers are far more likely to honor a committed southbound rate when the Florida backhaul is arranged at the same time, while one-way tenders remain vulnerable to late-day repricing.

Regional Insight

Charlotte-to-Chicago margin risk sits at the receiver, not on the linehaul

Chicago remains a favorable destination, but heat across Illinois and Missouri increases the odds of slower unloads, yard congestion, and evening rollover risk through Wednesday. On this lane, margin erosion is more likely to come from detention and missed appointment windows than from a sudden jump in buy rates, which makes drop-friendly capacity more valuable than shaving a few cents off linehaul.

📰 Breaking Down: Matson Q2 Earnings Highlight Robust Transpacific Demand

Matson's second-quarter 2026 financial results reveal a significant 16.7% year-over-year revenue growth to $969.4 million, driven primarily by robust demand in its China service. CEO Matthew Cox highlighted that tight market conditions and continued demand across e-commerce, garments, and e-goods were the primary factors behind this positive performance. This surge in transpacific container volumes has direct upstream implications for the domestic freight market, as the influx of ocean cargo will inevitably transition to domestic truckload and intermodal networks.

For domestic freight brokers, this sustained import volume at West Coast ports, particularly Los Angeles and Long Beach, will drive intense demand for outbound drayage, dry van, and intermodal capacity. As ocean carriers manage capacity tightly and spot rates remain elevated, the domestic spot market is likely to experience prolonged peak-season pressure. Brokers should expect outbound West Coast rates to remain firm, with capacity tightening as retail and e-commerce shippers rush to move imported goods to inland distribution centers.

Furthermore, Matson's expansion and integration in Southeast Asia suggest that supply chains are continuing to diversify, which will create new freight corridors and routing complexities. Brokers who specialize in port logistics and cross-border freight should closely monitor these volume shifts to position their carrier networks effectively. The strong operating margins reported by Matson indicate that shippers are willing to pay a premium for speed and reliability, a trend that brokers can capitalize on by offering high-service expedited solutions.

📊 Post-Weekend Volume Rebound Drives Spot Rate Firming

The domestic spot market experienced a sharp post-weekend volume rebound on Monday, August 10, 2026, with total available loads surging 12.5% overnight to 101,445. This influx of volume has driven the market average rate up to $2.83/mile, reflecting increased carrier pricing power as weekday shipping activity resumes. The data reveals a clear shift from the weekend contraction, with all major equipment types showing double-digit volume gains.

Reefer equipment saw the most dramatic volume surge, with available loads increasing 21.3% overnight to 7,473. This surge has pushed the average paid rate to $3.25/mile, representing a $0.15/mile carrier premium over posted rates. This tight capacity is driven by the collision of peak summer produce harvests and extreme heat warnings, which force carriers to demand higher rates to cover the risks of equipment failure and pre-cooling. Dry van volumes also rebounded by 11.3% to 20,470 available loads, with the average paid rate climbing to $2.68/mile, yielding a $0.10/mile carrier premium.

Flatbed equipment remains the largest segment of the active spot market, with available loads increasing 14.8% overnight to 36,534. Despite the high volume, flatbed rates show a tight $0.05/mile broker-favorable spread, with average posted rates at $3.09/mile and average paid rates at $3.04/mile. This suggests that while demand is robust, flatbed capacity remains relatively balanced, allowing brokers to maintain reasonable margins. However, extreme heat in the Southwest and West Coast could physically constrain open-deck capacity, potentially driving rates up in the coming days.

📅 Peak Summer Produce Harvests Strain Reefer Capacity

As of mid-August 2026, the domestic freight market is in the midst of peak summer produce harvests, which are driving intense competition for temperature-controlled capacity. Key commodities currently in transit include tomatoes from California and Ohio, peaches from South Carolina and Colorado, cantaloupes from California and Indiana, and grapes from California. These highly perishable, time-sensitive commodities require pre-cooled equipment and tight transit windows, placing immense pressure on outbound reefer supply from major agricultural regions.

This seasonal surge is particularly evident in California and the Southeast, where outbound reefer capacity is structurally tight and commanding significant rate premiums. Brokers managing temperature-controlled freight must act aggressively to secure equipment, as grocery distribution, food service, and pharmaceutical cold-chain networks are all competing for the same limited pool of reefer units. To mitigate this tight capacity, brokers should target inbound loads to these high-demand agricultural zones, offering carriers attractive return freight to negotiate favorable backhaul rates.

Over the next 7 to 14 days, this produce-driven demand is expected to remain high, keeping reefer rates elevated across the country. Additionally, extreme heat warnings in the Southwest and Midwest will continue to complicate operations, increasing the risk of reefer unit breakdowns and forcing carriers to demand higher premiums for temperature-sensitive loads. Brokers should advise shippers to expect extended lead times and higher transportation costs for refrigerated freight through the end of the month.

Strategic Takeaways

High-Signal Additions

- Refresh same-day spot quotes after noon; posted rates are lagging the live paid market.

- Bundle Atlanta-Florida loads with a confirmed return to protect coverage and limit reefer repricing.

- Use morning appointment windows in the Southwest and Kansas City metro wherever possible; weather risk is highest after midday.

- Watch for import-driven eastbound tightening out of Southern California later this week, especially on dry van.

🔑 Executive Signal Summary

- The market snapped back hard overnight: 101,445 total loads is a 12.5% increase from 90,179, and the national average rate jumped to $2.83/mile.

- The board is behind the live market: paid rates are above posted rates in van, reefer, heavy haul, specialized, and LTL (Less Than Truckload)/partial. Flatbed is the only category still showing buy-side room, and even there it is only $0.05/mile.

- Diesel at $5.299/gallon is keeping a real floor under capacity behavior: carriers are not tolerating unpaid deadhead, vague appointments, or soft reload visibility.

- Heat is tightening usable capacity more than posted capacity: the Southwest and Midwest are still moving freight, but they are moving it with more friction, more delay risk, and less patience for bad facilities.

- Today’s best brokers will win on timing, not just price: cover early, quote tighter, build the return leg first, and protect against afternoon repricing.

📊 What the market is really saying

This is a rebound in execution, not just a rebound in postings:

- 11,486 loads moved today versus 5,776 at the comparable time yesterday.

- That tells you the market did not simply post more freight; it started actually moving more freight.

Capacity is tighter than raw volume suggests:

- Today’s 101,445 loads are still below 108,741 from one week ago and below 117,492 from one month ago.

- But today’s average rate of $2.83/mile is higher than the $2.71/mile from one week ago and nearly back to the $2.85/mile from one month ago.

- Translation: you do not need record load volume to get firm pricing when diesel is high and operating friction is rising.

The national average is still industrial-weighted:

- Flatbed, heavy haul, and specialized total 66,144 loads, which is 65.2% of all posted loads.

- Those same segments account for 7,877 of 11,486 moved loads, or 68.6% of executed volume so far.

- Practical takeaway: do not let the $2.83 national average distort van or reefer buying. Those markets have their own behavior today.

The market is rewarding certainty:

- Carriers are getting paid up for appointment integrity, reload visibility, low dwell risk, and weather-aware timing.

- They are punishing freight with late pickups, unclear commodity details, outdoor loading in peak heat, and receiver congestion exposure.

🚚 Equipment-by-equipment broker playbook

1) Dry Van: tighter than the board looks

Market read:

- 20,470 loads

- $2.58/mile posted

- $2.68/mile paid

- $0.10/mile carrier premium

What it means:

- The posted market is lagging actual carrier expectation.

- Same-day and afternoon freight is especially vulnerable to repricing once carriers secure better reload options.

Broker move:

- Cover clean van freight early, especially outbound from the Midwest and Northeast.

- Shorten quote validity on same-day spot freight.

- Sell appointment precision to carriers, not just linehaul.

- Avoid detention-heavy facilities unless the customer agrees to pay for the risk.

Best use today:

- Retail and manufacturing freight with one pick/one drop, tight shipper communication, and credible destination reloads.

2) Reefer: service-first market, margin-second market

3) Flatbed: the only visible spread, but it is thin

Market read:

- 36,534 loads

- $3.09/mile posted

- $3.04/mile paid

- $0.05/mile broker-favorable spread

What it means:

- Yes, flatbed still shows some margin room.

- No, it is not easy money.

- Heat in the Southwest and West, plus loading friction across parts of the Midwest, can erase $0.05/mile very quickly through delay, tarping slowdown, or missed reloads.

Broker move:

- Take flatbed margin only on operationally clean freight.

- Confirm before quoting:

- tarping requirement

- securement detail

- loading method

- whether loading is indoor or outdoor

- realistic appointment time

- Favor morning pickups.

- Price detention early, especially on outdoor facilities.

Best use today:

- Shorter-turn flatbed freight with clean facility behavior and minimal staging uncertainty.

4) Heavy Haul: good demand, low forgiveness

Market read:

- 17,261 loads

- $3.28/mile posted

- $3.39/mile paid

- $0.11/mile carrier premium

What it means:

- Specialized project demand is still there.

- Carriers have leverage, and scope errors are expensive.

Broker move:

- Do not chase cheap specialized capacity with incomplete load detail.

- Confirm:

- dimensions

- weight

- axle requirements

- permits

- escorts

- route restrictions

- site loading and unloading conditions

Best use today:

- Freight where you already trust the customer and the job is fully scoped before posting.

Market read:

- 12,349 loads

- $3.02/mile posted

- $3.08/mile paid

- $0.06/mile carrier premium

What it means:

- The easy repositioning arbitrage from softer days is gone today.

- Specialized carriers can be selective.

Broker move:

- Use known carriers first.

- Post only fully described freight.

- Do not rely on vague commodity notes and expect the initial price to hold.

6) LTL/Partial: useful for density, not for aggressive rate cuts

Market read:

- 7,358 loads

- $1.68/mile posted

- $1.82/mile paid

- $0.14/mile carrier premium

What it means:

- This is not a soft partial market today.

- Carriers are still getting paid up for efficient consolidation and regional balance.

Broker move:

- Use LTL/partial to improve route density and customer stickiness.

- Do not sell it as a cheap alternative unless appointment flexibility exists.

- Keep partial networks tight around lanes where you already control volume.

Kansas City metro is a two-stage disruption market:

- Flash flooding around Johnson County, KS affects first-mile and local transfer reliability early.

- Then dangerous heat takes over later in the day.

- Morning pickup windows are far more reliable than afternoon handoffs.

Southwest heat is a duration problem, not a headline problem:

- The issue is not primarily road closure.

- The issue is:

- slower pre-cool cycles

- more idling

- reefer stress

- lower driver tolerance for late loading

- reduced practical Hours of Service (HOS)

Illinois, Missouri, and Kansas heat creates receiver-side risk:

- More yard congestion

- Slower unloads

- More detention disputes

- Higher odds of evening rollover

Broker move:

- Reprice afternoon pickups on heat-exposed freight now, not after the truck is on site.

- Ask for morning appointments first.

- Add buffer to same-day delivery promises through Wednesday on hot Midwest corridors.

🗺️ Regional money moves for the next 24–72 hours

1) Southeast: still the best place to make money if you control the loop

Why it matters:

- Produce keeps reefer tight.

- Retail and manufacturing keep van demand healthy.

- Capacity is not universally short, but it is selectively expensive where reload economics are weak.

Broker move:

- Think in round trips, not single legs.

- Pair inbound equipment with outbound freight from Georgia, South Carolina, and Florida.

- Protect your best carriers by giving them a next move, not just a first move.

2) Atlanta, GA → Orlando, FL: quote the return before you quote the southbound

3) Charlotte, NC → Chicago, IL: receiver risk is the real margin leak

What is happening:

- The linehaul is workable.

- The risk sits at destination because Midwest heat raises the chance of slow unloads, yard backlog, and appointment drift.

Broker move:

- Favor drop-capable or receiver-tolerant carriers.

- Widen delivery windows where possible.

- Do not underprice detention just because the linehaul looks stable.

4) Southern California eastbound: short buying window before import pressure spreads inland

What is happening:

- Strong transpacific demand and elevated ocean pricing usually tighten drayage and transload first, then eastbound van pricing a few days later.

- Heat makes that transition faster because it reduces truck productivity.

Broker move:

- Secure eastbound dry van coverage out of Southern California sooner rather than later.

- This is the kind of market where the cheapest truck at 8:30 AM is often unavailable by early afternoon.

🧠 The psychology in today’s market

Carrier psychology:

- Carriers are pricing uncertainty more aggressively than mileage.

- They care most about:

- how long they will sit

- whether reload is real

- whether the broker sounds organized

- whether accessorials will become an argument later

Broker advantage:

- A broker who can say, “morning pickup, pre-cooled, two-hour load window, detention addressed, return option available” will buy better than a broker who simply says, “What’s your truck need?”

Customer psychology:

- Some shippers will see more loads on the board and assume rates should fall.

- Today, that logic is incomplete.

- Board volume is up, but paid execution is firmer almost everywhere.

Best customer message:

- Generic freight is negotiable. Timing-sensitive freight is not.

- That distinction helps protect margin without sounding defensive.

🛡️ Risk controls to put in place before noon

1) Tighten quote validity

- Reefer, same-day van, Southern California outbound, and Florida freight should have shorter validity windows than normal.

- Afternoon market drift is a real threat today.

2) Score facilities before scoring lanes

- A mediocre lane with a fast shipper and receiver is safer than a “good lane” with chronic dwell.

- Facility behavior is deciding margin more than geography on many loads today.

3) Break out the rate components

- Separate:

- linehaul

- fuel

- temperature-service premium

- after-hours loading

- detention risk

- This makes repricing cleaner and reduces customer pushback.

4) Build one backup earlier than usual

- On reefer, produce, same-day, or weather-exposed freight, your backup truck should be identified before the primary truck checks in.

5) Reconfirm compliance on premium freight

- High-cost days attract desperate trucks.

- Recheck:

- authority

- insurance

- safety

- equipment type

- ELD (Electronic Logging Device) readiness

6) Protect the receiver

- Ask harder questions about unload speed and appointment discipline.

- On several lanes today, the receiver is a larger profit risk than the pickup.

📈 Probability-weighted outlook for the next 24–72 hours

50% — Selective firmness continues

- Van stays tighter than the board.

- Reefer remains clearly carrier-led.

- Flatbed keeps some margin room, but only on clean freight.

- Heat continues to degrade afternoon performance.

35% — Market tightens further by midweek

- Rising OTRI (Outbound Tender Rejection Index) and import pull from the West Coast push more freight into the spot market.

- Southern California eastbound van and Southeast reefer get more expensive first.

15% — Rebound fades into a more balanced Tuesday/Wednesday

- Even in this softer case, $5.299 diesel should prevent a real rate break on reliable capacity.

- The downside is limited unless weather eases and shipper urgency drops at the same time.

✅ Today’s priority stack

- Cover reefer and heat-exposed freight first

- Treat van posted rates as stale until proven otherwise

- Use flatbed spreads only on clean, morning, low-friction freight

- Sell Florida and produce lanes as network problems, not one-leg transactions

- Protect receiver-side detention on Midwest deliveries

- Secure Southern California eastbound options before the afternoon market

- Shorten quote windows and refresh same-day spot prices after noon

- Do not dispatch premium freight without confirmed appointments, accessorial terms, and a backup plan

📏 Desk scorecard for a strong day

Coverage timing:

- Aim to cover most reefer and weather-sensitive loads before late morning local time.

Quote discipline:

- Every premium load should have clear validity language and separate accessorial treatment.

Facility discipline:

- No hot, same-day, or temp-sensitive load should move without confirmed shipper and receiver expectations.

Network discipline:

- Atlanta-Florida and major produce-related freight should be matched with return-leg thinking before dispatch.

Margin discipline:

- The goal is not just buying the cheapest truck.

- The goal is buying the truck most likely to hold the rate, hit the appointment, and preserve your second turn.

🎯 Bottom line

This is a firmer live market than the load board alone suggests.

Reefer is tight, van is tightening, flatbed still offers selective margin, and weather is making timing matter more than headline volume.

If you cover early, sell certainty, and build reloads before problems appear, today is a strong brokerage day.

💡 Tony's Tip

Please set up multi-factor authentication (MFA) on your ETA email account this week.

Visit

https://aka.ms/mfasetup to get started.

Text Tony at 205-876-3715 if you have any issues.

Also, please note, you should be using

https://freightmap.remote.etaagencyinc.com for google maps lookups so we dont get rate limited by Google.

You can check routes on the operations panel on the left via the red Check Route button.

📅 This Day in History

1904: Russo-Japanese War: The Battle of the Yellow Sea between the Russian and Japanese battleship fleets takes place.

1954: At Massena, New York, the groundbreaking ceremony for the Saint Lawrence Seaway is held.

1971: The Society for American Baseball Research is founded in Cooperstown, New York.

💭 Quote of the Day

"Success is not final, failure is not fatal: it is the courage to continue that counts."

— Winston Churchill